Introduction

Debt doesn’t just affect your bank account. It follows you into conversations you’d rather avoid, keeps you up at 2 a.m., and quietly reshapes the way you think about the future.

If you’ve been searching for debt relief, chances are you’re dealing with more than a few overdue statements. Maybe it’s credit card balances that keep climbing despite your monthly payments. Maybe it’s medical bills that arrived without warning, or personal loans that made sense at the time but feel impossible now.

You’re not alone. Millions of Americans are in the exact same position heading into 2026, and many of them are actively looking for a way out that doesn’t involve a miracle or a lottery ticket.

The good news: there’s no single solution to debt, which actually works in your favor. Different strategies suit different situations, and understanding your options puts you in a much stronger position than ignoring the problem and hoping things improve on their own.

This guide covers nine of the most practical debt relief options available right now, what each one actually involves, and how to figure out which path makes the most sense for your situation.

What Is Debt Relief, Really?

The term “debt relief” gets used loosely, but at its core, it refers to any structured approach that makes your debt easier to manage, reduces what you owe, or helps you pay it off more efficiently.

That can mean a lot of different things depending on who you talk to:

- Lowering your interest rate so more of your payment goes toward the principal

- Combining multiple accounts into a single monthly obligation

- Negotiating with creditors to accept a reduced payoff amount

- Following a disciplined repayment method that actually works

- In rare cases, pursuing legal protection through bankruptcy

The goal isn’t to make debt disappear overnight. It’s to create a realistic, workable plan one that fits your income, your lifestyle, and where you want to be financially in the next few years.

Before you settle on any strategy, take stock of three things: your total debt load, what you can realistically put toward repayment each month, and whether your income situation is stable. Those three factors will shape everything else.

Why Debt Relief Is a Growing Priority in 2026

This isn’t a new problem, but several conditions have made it more urgent for a wider range of people.

Interest rates on credit cards remain high, which means carrying a balance costs significantly more than it used to. At the same time, everyday expenses groceries, utilities, insurance have risen steadily, leaving less room in household budgets. Medical expenses continue to be one of the leading contributors to personal debt, often arriving suddenly and without much recourse.

Student loan obligations haven’t gotten easier. And for many households, emergency savings that once provided a cushion simply aren’t there anymore.

The result is that people who were managing their debt just fine a few years ago are now finding it harder to stay current. The earlier you start exploring your options, the more of them remain available to you.

Signs That You May Need Debt Relief

Not every financial rough patch calls for a formal debt relief strategy. But certain patterns are worth paying attention to.

Your minimum payments aren’t making a dent. If you’re consistently paying the minimum and your balance barely moves, high interest is likely consuming most of what you’re sending in.

You’re using credit cards to cover essentials. When groceries, gas, and utility bills start going on a card because cash isn’t available, that’s a signal that expenses and income are out of alignment.

Collection calls have started. Frequent contact from debt collectors typically means accounts have gone delinquent — and the situation will keep escalating without action.

Your credit score is sliding. Missed payments and high utilization both drag scores down. A declining score can also limit your options going forward, so addressing it earlier is generally better. If you’re also looking to rebuild your credit profile while reducing debt, check out our guide on How to Improve Credit Score Fast: 25 Proven Ways That Actually Work for practical strategies that can help strengthen your score over time.

The stress is becoming constant. Financial anxiety that affects your sleep, your relationships, or your ability to concentrate at work isn’t something to push through indefinitely. It’s a sign the underlying issue needs attention. If money worries are starting to affect your daily life, our guide on Coping With Financial Stress: What to Do When the Anxiety Won’t Stop offers practical ways to manage the emotional side of financial pressure.

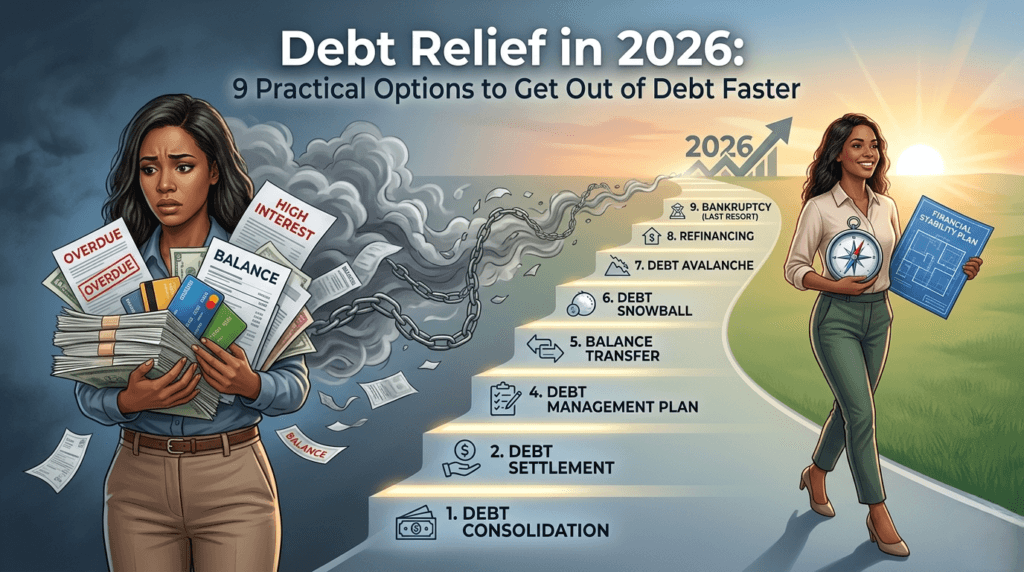

The 9 Debt Relief Options Worth Considering

1. Debt Consolidation

Debt consolidation takes several separate balances and rolls them into a single loan with one monthly payment. Instead of tracking four or five accounts with different due dates, interest rates, and minimum requirements, you’re managing one.

Done right, consolidation can also lower your overall interest rate particularly if your existing debt is spread across high-rate credit cards.

It works best when you still have decent credit (lenders need to approve the new loan), a steady income, and the discipline to avoid adding new balances after consolidating. It doesn’t solve the spending habits that may have contributed to the debt in the first place.

2. Debt Settlement

Settlement is a negotiation you or a company acting on your behalf approaches a creditor and proposes paying a lump sum that’s less than the total balance owed. Creditors sometimes agree, particularly on accounts that have been delinquent for a while, because some recovery is better than none.

A creditor might, for example, agree to close out a $9,000 account for a one-time payment of $5,500.

There are real tradeoffs here. Settlement typically requires that accounts be in arrears before creditors will negotiate, which means your credit score takes a hit in the meantime. The forgiven amount may also count as taxable income, which catches some people off guard. Settlement makes the most sense when other options are off the table and there’s a clear path to getting out.

3. Credit Counseling

Working with a nonprofit credit counseling agency gives you access to someone who can look at your full financial picture — income, debts, spending patterns — and help you build a realistic plan.

Counselors typically assist with budgeting, organizing your debt by type and interest rate, and developing a structured path forward. Many agencies charge little or nothing for this service, making it one of the more accessible starting points.

If you’re unsure where to begin or feel overwhelmed by the scope of the problem, credit counseling is often the right first step.

4. Debt Management Plans

A Debt Management Plan, or DMP, is usually offered through a credit counseling agency and is a step beyond counseling. Under a DMP, your multiple debts are consolidated into a single monthly payment managed by the agency, which distributes funds to your creditors. In many cases, creditors agree to reduce interest rates or waive certain fees as part of the arrangement.

DMPs typically run three to five years and require that you stop using the accounts included in the plan. They’re best suited for people with multiple credit card balances who want structure and external accountability to help them follow through.

5. Balance Transfer Credit Cards

If your credit score is strong enough to qualify, a balance transfer card with a 0% introductory APR can be a practical tool. You move high-interest balances to the new card and pay them down during the promotional window — often 12 to 21 months — without accumulating more interest.

The catch is that the promotional rate eventually expires, and any remaining balance will start accruing interest at the card’s standard rate, which may be high. This strategy works well for disciplined borrowers who have a concrete payoff plan and won’t be tempted to run the balance back up.

6. Debt Snowball Method

The snowball method is a DIY repayment strategy. You line up your debts from smallest balance to largest, make minimum payments on everything, and put every extra dollar toward the smallest one first. Once that’s paid off, you roll that payment into the next smallest balance.

The appeal is psychological. Paying off a full account even a small one provides a clear sense of progress that can motivate you to keep going. It may not save the most money in interest compared to other methods, but it works well for people who benefit from visible, early wins.

7. Debt Avalanche Method

The avalanche method follows the same basic structure as the snowball, but prioritizes debts by interest rate instead of balance size. You attack the highest-rate debt first, then move down the list.

Mathematically, this approach saves more money over time because you’re eliminating the most expensive interest charges as quickly as possible. The tradeoff is that progress can feel slow in the beginning if your highest-rate debt also happens to be your largest balance. It tends to work best for people who are motivated by efficiency rather than quick emotional wins.

8. Refinancing Existing Loans

Refinancing replaces an existing loan with a new one that carries better terms typically a lower interest rate, a lower monthly payment, or both. It’s commonly used for personal loans, auto loans, and student loans.

This can meaningfully reduce your monthly obligations and the total amount you pay over time. Like consolidation, it generally requires solid credit and stable employment to qualify. It’s worth revisiting if your credit profile has improved since you originally took out a loan, as you may now qualify for significantly better rates.

9. Bankruptcy as a Last Resort

Bankruptcy carries serious, lasting consequences — it stays on your credit report for seven to ten years and affects your ability to borrow, rent, or sometimes even get hired. That’s why it should only be considered after other options have been genuinely exhausted.

That said, for people facing an overwhelming debt load with no realistic path forward, bankruptcy provides legal protection from creditors and a defined process for either discharging certain debts (Chapter 7) or restructuring them (Chapter 13). It’s not a failure it’s a legal mechanism that exists precisely for situations of genuine financial hardship.

Always consult a qualified bankruptcy attorney before making this decision. The specifics matter enormously, and an attorney can help you understand exactly what you’d be giving up and gaining.

How to Choose the Right Option for Your Situation

The debt relief strategy that works for your neighbor or your coworker may not be right for you. Here’s a simplified framework:

If your credit is still in good shape: Debt consolidation or a balance transfer card can lower your interest rate while you pay down balances efficiently.

If you’re behind on payments: Credit counseling or a Debt Management Plan can provide structure, accountability, and potentially improved terms from creditors.

If the debt feels genuinely unmanageable: Debt settlement is worth exploring once you’ve reviewed everything else. Go in with realistic expectations about the credit impact.

If you’re facing severe financial hardship: A bankruptcy attorney can walk you through what that process actually looks like and whether it applies to your situation.

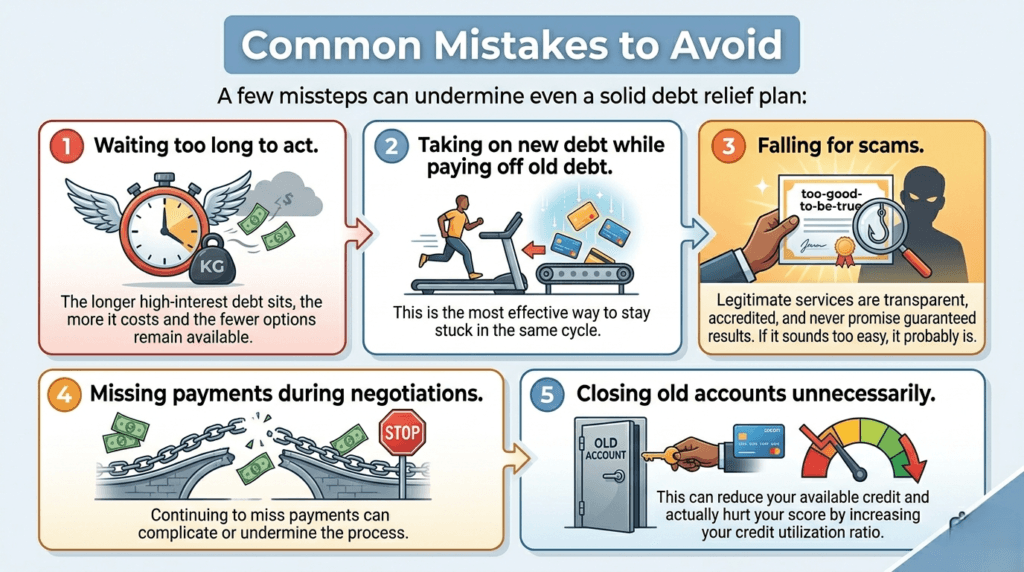

One thing that applies across the board: whatever strategy you choose needs to address not just the existing debt, but the conditions that created it. A plan that doesn’t account for spending habits or income challenges is unlikely to hold.

Final Thoughts

Debt has a way of feeling permanent, like something you’ll always be carrying. But most people who take a structured approach — and stick with it — make meaningful progress faster than they expected.

The most important thing isn’t choosing the perfect strategy on day one. It’s making a realistic decision based on your actual situation and then following through consistently. Small, steady progress compounds over time in ways that are hard to appreciate when you’re just getting started.

If you’ve been sitting with this problem and waiting for the right moment to deal with it, this is probably a reasonable time to stop waiting. The options available to you now may not all be available six months from now, depending on how your credit and financial situation evolve.

Start with an honest look at what you owe, what you can realistically pay each month, and which of the nine options outlined here fits that picture. Then take one step — just one — today.

Financial stability isn’t out of reach. It’s just further away when you’re standing still.

Frequently Asked Questions

There isn’t a universal answer. Debt consolidation tends to work well for people with good credit who want a simplified repayment structure. Credit counseling and DMPs are better suited to those who need guidance and accountability. The right option depends almost entirely on your specific financial situation.

Some methods will, at least temporarily. Debt settlement in particular typically requires accounts to fall delinquent before creditors will negotiate, which affects your score. Other approaches like a DMP or consolidation have a smaller impact, and consistent on-time payments will help your score recover over time.

They serve different purposes. Consolidation simplifies repayment and may reduce interest costs it works best when you’re still current on payments and have stable income. Settlement reduces the amount you actually owe, but involves a more significant short-term credit impact and is typically used when normal repayment isn’t feasible.

Yes. DMPs, credit counseling, the snowball method, and the avalanche method don’t require borrowing additional money. They work with what you already owe.

It varies considerably. Some people make significant progress within a year. Others particularly those with larger balances or lower incomes may need several years to fully work through their debt. Consistency matters more than speed.

In some circumstances, yes. Formal programs, legal protections, and negotiated agreements can reduce or eliminate collection activity. Results vary based on the specific strategy and the creditor involved.

Not automatically. Many legitimate companies provide real value, but the space also includes operators that charge high fees and make promises they can’t keep. Before signing anything, verify the company’s accreditation, read the fee structure carefully, and look at independent reviews.

Absolutely most programs are specifically designed for it. High-interest credit card balances are the most common reason people seek debt relief, and consolidation, balance transfers, and repayment plans are all well-suited to addressing them.

Thanks a lot for sharing this with all folks you actually realize what you are

talking about! Bookmarked. Please additionally seek advice from my website =).

We could have a link change agreement between us

yes, please share the details