Introduction

Not long ago, asking whether artificial intelligence was worth investing in felt like a niche question reserved for tech insiders and venture capitalists. Now it’s something your coworker is debating at lunch, your financial advisor is fielding calls about, and CNBC is covering around the clock.

That kind of rapid mainstream attention is exciting. It’s also exactly the kind of thing that has preceded some of the most painful market corrections in recent history.

So here’s the real question: Is the surge in AI investment a genuine, fundamental shift in how the economy works — or are we watching the early stages of a bubble that will eventually pop?

The honest answer is that it’s probably some of both. And knowing which parts are which is what separates a smart investment decision from an expensive one.

This piece isn’t here to hype AI or dismiss it. It’s here to give you a clear, grounded picture of where things stand in 2026 — the risks that are real, the opportunities that are legitimate, and how to think about all of it as an American investor trying to make sound decisions.

What Actually Makes a Market Bubble

Before deciding whether AI qualifies, it helps to understand what a bubble actually is — not the pop-culture version, but the mechanics of how it forms and why it eventually falls apart.

A bubble happens when asset prices rise substantially beyond what the underlying business or asset can reasonably support. Investors stop asking “what is this company actually worth based on its earnings, cash flow, and competitive position” and start asking “how much will someone else pay for this tomorrow?”

That shift — from valuation to momentum — is the defining feature of a bubble. It’s not about excitement or enthusiasm per se. It’s about the point at which price becomes disconnected from reality in a way that can’t be sustained indefinitely.

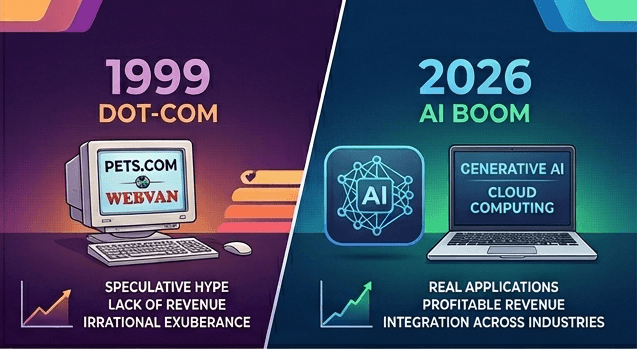

The dot-com era is the textbook case. Investors weren’t wrong that the internet would transform the world. They were wrong that almost every company racing to plant a flag online would become a profitable, durable business. Most didn’t. Prices had run so far ahead of earnings — in many cases, ahead of any revenue at all — that a correction wasn’t just possible. It was inevitable.

That framing matters here because the question with AI isn’t whether the technology is real or important. It clearly is. The question is whether the prices investors are paying today reflect realistic expectations or something much more optimistic.

What’s Driving the Surge in AI Investment

The enthusiasm around AI isn’t coming from nowhere. Several concrete factors have pushed AI-related stocks and valuations to where they are today.

Corporate spending is substantial and growing. This isn’t a trend on paper. Companies are committing real money to AI infrastructure — data centers, cloud capacity, software platforms, automation tools. When large enterprises allocate billions to a technology, it’s because they expect measurable returns, not because a trend piece told them to.

Early productivity gains are visible. Developers are writing and debugging code faster. Customer service operations are handling higher volumes at lower cost. Marketing teams are producing content more efficiently. Legal and finance teams are processing documents in a fraction of the time. These aren’t hypothetical benefits — they’re showing up in operational metrics at companies across industries.

Capital is looking for a home. Financial markets are always hunting for the next durable growth story. After several years of choppy returns in other sectors, AI has become the clearest narrative around which large amounts of investment capital can organize. That creates its own momentum, separate from the fundamentals.

The enabling infrastructure is already built. Unlike previous technology transitions that required consumers or businesses to completely change behavior, AI is layering onto infrastructure that already exists. The cloud is there. The devices are there. The data is there. The friction to adoption is lower than it was for the internet in 1997.

The Case That a Bubble Is Forming

With all that said, there are serious and legitimate reasons to be cautious — and dismissing them as pessimism misses the point.

Valuations Have Gotten Very Aggressive

This is the most straightforward concern. Many AI-related companies are priced to near-perfection, meaning they need to continue delivering exceptional growth just to justify where they’re trading today, let alone move higher.

When a company’s stock price assumes five to ten years of rapid, uninterrupted growth, any deviation — a slower quarter, a new competitor, an unexpected cost — can produce significant declines. That’s not a flaw in the technology. It’s a function of how expensive the expectation has become.

Emotional Buying Is Clearly Present

Every bubble involves a period where people invest not because they’ve done careful analysis, but because they’re afraid of being left behind. That dynamic is visibly present in AI right now. Social media, financial influencers, and relentless news coverage create real psychological pressure to participate — regardless of whether the price makes sense.

Before making investment decisions based on market excitement, it’s worth reviewing our guide on Smart Money Is Moving While Everyone Else Is Just Spending.

The Startup Landscape Is Crowded and Undifferentiated

When a technology generates this much excitement, thousands of companies rush to attach themselves to it. Some of these businesses have genuine technology, real competitive advantages, and viable paths to profitability. Many others are essentially repackaging existing tools with an “AI-powered” label and riding the wave.

Historically, only a small fraction of companies that emerge during a technology boom become lasting winners. Identifying which ones before the market sorts it out is genuinely difficult.

Real-World Adoption Is Slower Than Headlines Suggest

AI is powerful, but deploying it at scale inside complex organizations is hard. Integration takes time. Employees need training. Existing systems need to be retrofitted. Compliance and regulatory questions need to be addressed. The gap between what AI can do in a controlled demo and what it actually contributes to a company’s bottom line this quarter can be significant.

When investor expectations run ahead of adoption timelines, that gap eventually has to close — usually in the form of disappointing earnings.

The Case That AI Is Different This Time

The bubble concerns are real, but so is the other side of the argument. And there are several meaningful differences between where AI stands today and where previous speculative bubbles stood at their peaks.

Today’s Leading AI Companies Are Profitable

This is probably the most important distinction from the dot-com era. Many of the companies at the center of the AI story — the hyperscalers, the enterprise software platforms, the chip manufacturers — are generating substantial, real revenue. Some are among the most profitable businesses in history.

That doesn’t make them immune to overvaluation. But it does mean the floor underneath these companies is significantly more solid than it was for a company with no revenue and a “.com” at the end of its name in 1999.

The Technology Is Already Delivering Measurable Value

AI isn’t a promise waiting to be fulfilled. It’s already reducing costs, improving efficiency, and creating new capabilities across healthcare, finance, manufacturing, logistics, legal services, and dozens of other sectors. Technologies that demonstrably help businesses and consumers tend to persist through market cycles, even when valuations temporarily correct.

Enterprise Demand Is Structural, Not Speculative

The biggest spenders on AI aren’t retail investors chasing a trend. They’re hospitals implementing AI diagnostics. Banks running AI-driven fraud detection. Retailers optimizing supply chains. Manufacturers improving quality control. These are capital allocation decisions made by large organizations with rigorous ROI requirements.

That kind of demand doesn’t evaporate because a stock index pulls back.

AI Is Likely to Become Infrastructure

The comparison to electricity or the internet gets made often enough that it can start to sound tired, but it’s worth taking seriously. The technologies that became truly transformative didn’t stay in a single industry — they became the layer on which everything else ran.

If AI follows that trajectory, the current moment may eventually look less like a bubble and more like the early stages of a very long structural shift. That doesn’t mean every company participating in that shift will thrive. Many won’t. But the underlying technology may prove more durable than skeptics expect.

AI vs the Dot-Com Bubble: An Honest Comparison

The parallel keeps getting drawn, so it’s worth being specific about where it holds and where it breaks down.

What’s similar: Both created enormous investor excitement. Both attracted waves of startup activity. Both prompted serious people to predict the technology would reshape the entire economy. Both pushed valuations to levels that assumed extraordinary future growth.

What’s different: In the late 1990s, a meaningful portion of dot-com companies had no revenue, no clear path to profitability, and business models that didn’t make economic sense at any scale. Today’s AI leaders are largely mature businesses with real earnings. The speculation is real, but it’s layered on top of actual value in a way that wasn’t true during the dot-com peak.

The takeaway isn’t that AI can’t correct sharply — it can and some parts of it likely will. The takeaway is that the comparison isn’t as clean as it’s often presented, and applying dot-com logic wholesale to the AI landscape probably overstates the downside risk in established companies while potentially understating it in early-stage players.

What to Actually Watch If You’re an Investor

Whether you’re already holding AI positions or thinking about getting in, these are the signals worth monitoring — not the daily price movements or the latest earnings beat narrative, but the underlying fundamentals that actually determine long-term value.

Revenue quality. Is AI revenue growing because customers are genuinely getting value, or because companies are signing deals to look current? Retention rates and expansion revenue are more informative than new contract announcements.

Path to profitability. For earlier-stage AI companies, the question isn’t whether they’re growing — it’s whether they can grow into a business model that actually makes money. Burn rate and margin trajectory matter.

Competitive moat. AI tools are becoming commoditized quickly. Companies that have advantages rooted in proprietary data, deep customer integration, or regulatory relationships are better positioned than those competing purely on model quality, which changes constantly.

Regulatory environment. The US and EU are both in the early stages of establishing AI governance frameworks. How those develop over the next two to three years will affect which business models remain viable and at what cost.

Capital expenditure sustainability. The buildout of AI infrastructure — particularly data centers and chips — requires enormous ongoing investment. Tracking whether that spending is generating proportional revenue growth is important.

What Should Regular Investors Actually Do?

This is where most financial coverage gets either overly cautious or recklessly optimistic, so here’s a straightforward take.

IInvestors looking to strengthen their overall financial position should also focus on managing debt and improving cash flow. Our guide on Debt Relief in 2026: 9 Practical Options to Get Out of Debt Faster explains several strategies that can help.. You’re participating in the upside without concentrating risk in companies that might not exist in five years.

If you’re considering significant positions in individual AI stocks — particularly early-stage companies or startups — the risk profile is meaningfully different. Some will generate exceptional returns. Many won’t. The ability to identify which is which requires research that goes well beyond what’s covered in financial media.

What most investors should avoid: chasing performance after a strong run, making large allocation changes based on news coverage, and treating AI stocks as a guaranteed way to capture the technology’s importance. A transformative technology and a good investment are not the same thing. The dot-com era proved that conclusively.

Diversification, realistic time horizons, and decisions grounded in fundamentals rather than momentum are not exciting advice. They’re also the approach that tends to hold up when things get turbulent.

Final Thoughts

The AI bubble question doesn’t have a clean answer, and anyone who tells you otherwise is either oversimplifying or selling something.

There are real signs that parts of the AI market have gotten ahead of themselves. Valuations in some corners are aggressive. Speculation is present. And when investor expectations are this high, disappointment doesn’t need to be dramatic to cause significant price declines.

At the same time, the technology is genuinely producing value. Businesses are adopting it not because it’s fashionable but because it’s working. The companies at the center of the AI buildout are, in many cases, financially strong in ways that dot-com companies simply weren’t.

The most useful frame for American investors right now is probably this: AI as a technology is likely here to stay and will continue to matter. AI as an investment requires the same discipline you’d apply to anything else — understanding what you’re buying, what you’re paying for it, and whether the price reflects reality or expectation.

The two things are easy to conflate when everyone around you seems to be getting rich. They’re worth keeping separate.

Frequently Asked Questions

There are genuine signs of speculation in certain parts of the AI market, particularly in early-stage companies and some highly valued stocks. But the leading AI companies have real revenue and real earnings, which distinguishes this from classic bubble conditions. A correction is possible — particularly if growth disappoints — but a wholesale collapse similar to the dot-com crash seems less likely given the underlying fundamentals.

Companies with high valuations, minimal revenue, and business models that depend entirely on AI enthusiasm rather than sustainable competitive advantages carry the most risk. Early-stage startups and companies that have repositioned themselves as “AI companies” without substantive technology changes are worth scrutinizing carefully.

That depends entirely on your specific holdings, overall portfolio, time horizon, and risk tolerance. In general, panic-selling based on fear of a correction isn’t a sound strategy any more than buying based on fear of missing out. If you’re uncomfortable with your current exposure, gradual rebalancing is usually more prudent than large sudden moves.

In some meaningful ways, yes. The scale of real revenue generated by today’s leading AI companies is substantially larger than what existed during the dot-com peak. That said, portions of the AI market — particularly certain startups and high-multiple growth stocks — share characteristics with dot-com speculation. It’s not a binary question.

Broad exposure through diversified technology index funds, focusing on established companies with strong balance sheets, and avoiding concentration in speculative names are all reasonable approaches. If you’re considering individual AI stocks, thorough research into fundamentals — not just growth narratives — is essential.